The concept of retirement is changing, with fewer people working towards a final retirement date and then clocking off for good.

Instead, those who have the flexibility to choose are often transitioning out of the workforce over several years, or even returning after a break.

Whether you simply want to wind back your working hours to explore other interests, or don’t want to cut your ties with work completely, to make it work you will need to plan ahead.

Choosing your retirement date

If you want to retire in the next few years, you need to work out how you will finance your living expenses once you no longer receive a regular wage or salary.

There is no set retirement age in Australia, but most people will not be eligible to receive an Age Pension until they reach age 67.i This means you will need enough savings to provide another income source if you hope to retire earlier.

Although most of us have super, you are not permitted to access it until you reach your preservation age, which is currently 59 and soon to increase to age 60 depending on when you were born.ii

Withdrawing your super also requires you to meet a condition of release. There are various conditions, but the most common one is reaching age 60 and permanently retiring from the workforce. Once you turn 65, you can access your super whether you are working or not.

Keep in mind, tax also affects your super, with different rates applying depending on whether you have reached your preservation age, or are aged 60 and over. Most people can access their super savings tax-free once they reach 60.

Paying for your retirement

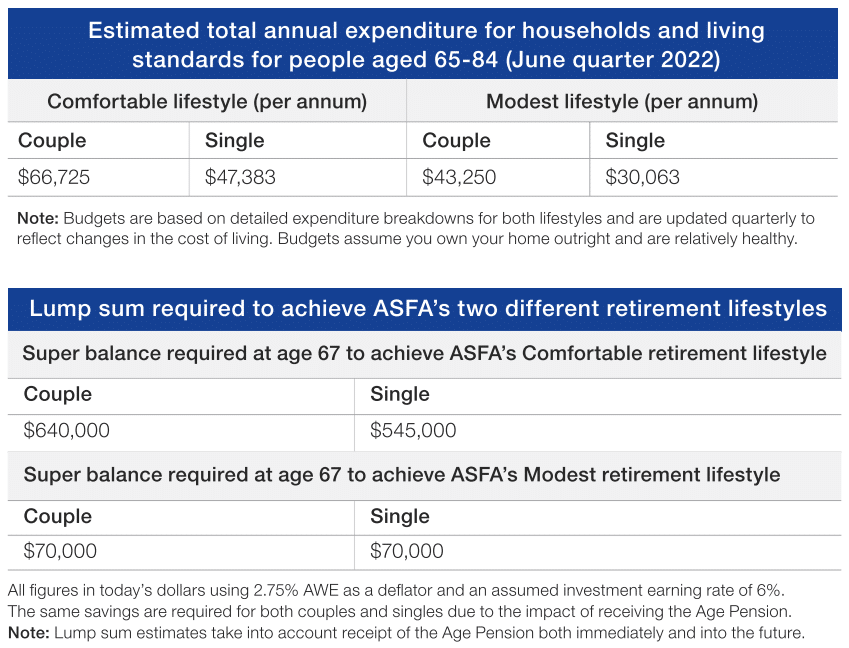

Unfortunately, there is no simple answer to how much income you will need in retirement. It depends on your current lifestyle and planned retirement activities, but a good place to start is the ASFA Retirement Standard (see table).

For around 62% of the population aged 65 and over, the main source of retirement income is the Age Pension and government payments.iii

Eligibility for an Age Pension is assessed using your age, residency status and personal income and assets. These determine whether you receive the full fortnightly payment rate, which is currently $1547.60 for a couple.

As part of your planning, check for other potential sources of income you can use if you retire fully, or decide to slowly transition. Possibilities could include income from investment assets, contract work, or rent from investment or Airbnb properties.

Using your super savings

While you may dream of retiring early, many of today’s retirees can expect to live well into their 80s so, your super may need to provide income for more than 20 years.

If you are unsure whether your super is on track, most super funds provide online calculators to give a rough estimate of your likely retirement balance and how much income it will provide.

ASIC’s MoneySmart Retirement Planner is another useful tool for working out your retirement income and potential Age Pension payments. It also illustrates how extra super contributions and changing investment options could affect your final balance.

Transition-to-retirement (TTR) pensions

If you would like to ease into retirement, it can be worth investigating a TTR pension. These allow you to cut back your working hours while using your super to supplement your income without compromising your lifestyle.

If you are aged 55 to 59 you will pay some tax on these pension payments, but they are tax-free once you reach age 60.iv

TTR pensions also allow you to continue topping up your super through a salary sacrifice arrangement with your employer. You only pay 15% tax on these contributions, which may be lower than your marginal tax rate.

Giving super a late boost

If you have income to spare as you move towards retirement, perhaps from an inheritance or downsizing your home, there are now additional opportunities to continue adding to your super.

You can make personal after-tax contributions of up to $110,000 a year until you reach age 75, even if you are not working. You may even be eligible to use a bring-forward arrangement and add up to $330,000 in a single year. in a single year.

Once you hit 60, if are planning to sell your current home you can also make a downsizer contribution of up to $300,000 ($600,000 for a couple) into your super account.

The role of home ownership

Despite falling levels of home ownership, most people still aspire to being debt-free free by the time they retire with a home fully paid for or close to it.

Your home could even be a source of retirement income, using a reverse mortgage or the government’s Home Equity Access Scheme.

When you are doing your retirement sums, don’t forget some of the concessions on offer to older Australians. If you are aged 60 and over and working less than 20 hours per week, your state’s Seniors Card can provide discounts on public transport and some goods and services.

You may also be eligible for the Commonwealth Seniors Health Card for cheaper prescriptions and medical appointments, or a Pensioners Concession Card for discounted public transport.

Estimating how much you are likely to need in retirement

As everyone’s financial position and retirement plans are different, it’s impossible to predict exactly how much you will need when you retire. But a useful starting point can be the Association of Superannuation Funds in Australia’s Retirement Standard, which estimates the income required to support two different retirement lifestyles.

If you would like to discuss your retirement options and how to fund them, give us a call.

i https://www.servicesaustralia.gov.au/who-can-get-age-pension?context=22526

ii https://www.ato.gov.au/Individuals/Super/

iii https://www.aihw.gov.au/reports/australias-welfare/age-pension

iv https://moneysmart.gov.au/retirement-income/transition-to-retirement