Since August 1 the top 200 companies in Australia, the ASX 200, are down over 9.1%. The top 500 companies in America, the S&P 500, is down 10.4% which is considered a ‘correction’. This is normal and nothing to panic about. We live in a world of uncertainty and volatility.

Economically we are still dealing with a COVID hangover. In this email I am going to go through a couple of key points that will help you understand what is going on in the world, and then the proven investment principles to apply in the current environment.

We will discuss:

- Share markets as leading indicators

- Interest rates

- Inflation

- Hard landing vs. Soft landing

- Market volatility & Timing the Market

- The Unpredictability of Returns

- Cash is King isn’t it

- Annual share market returns and intra-year volatility

- What long term investing looks like

- What we are doing on the investment front

1. Share markets as economic leading indicators

Share markets are a leading economic indicator, typically ‘forward looking’ around 6-12 months so this is telling us that economic conditions are going to get a little bit tougher.

And this is exactly what central banks want globally!!

There is a global balancing act happening between interest rates and inflation.

2. Interest rates

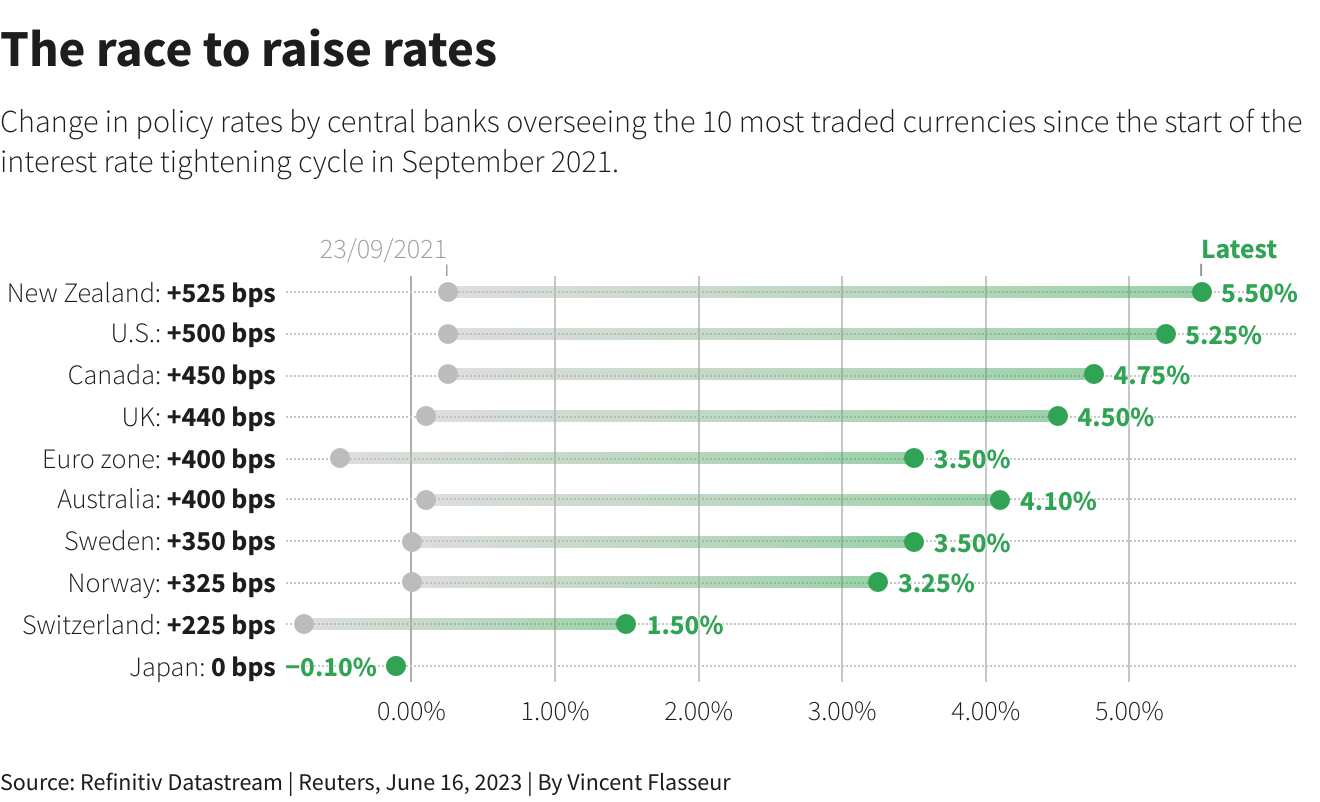

Interest rates have gone up drastically since the start of 2022 to try and slow down the global economy. The chart below shows the change in policy rates by central banks since the start of the interest rate tightening cycle in September 2021. These are some of the fastest rate hikes in history as central banks try to unwind the inflation that were rooted in government responses to COVID i.e. putting more money in the system, historically low interest rates, to stave off an economic depression, which many thought possible at the time.

3. Inflation

The goal of central banks raising rates is to cool inflation. Federal Reserve chairman Jerome Powell acknowledged recent signs of cooling inflation but said the central bank would be ‘resolute’ in its commitment to its 2% mandate. Interestingly as he spoke (23/10/2023) the futures trading market erased the possibility of a rate hike in November and decreased the chances in December.

Powell said the following at a speech at the Economic Club of New York:

“Inflation is still too high, and a few months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal,”

“We cannot yet know how long these lower readings will persist, or where inflation will settle over coming quarters.”

“While the path is likely to be bumpy and take some time, my colleagues and I are united in our commitment to bringing inflation down sustainably to 2 percent”

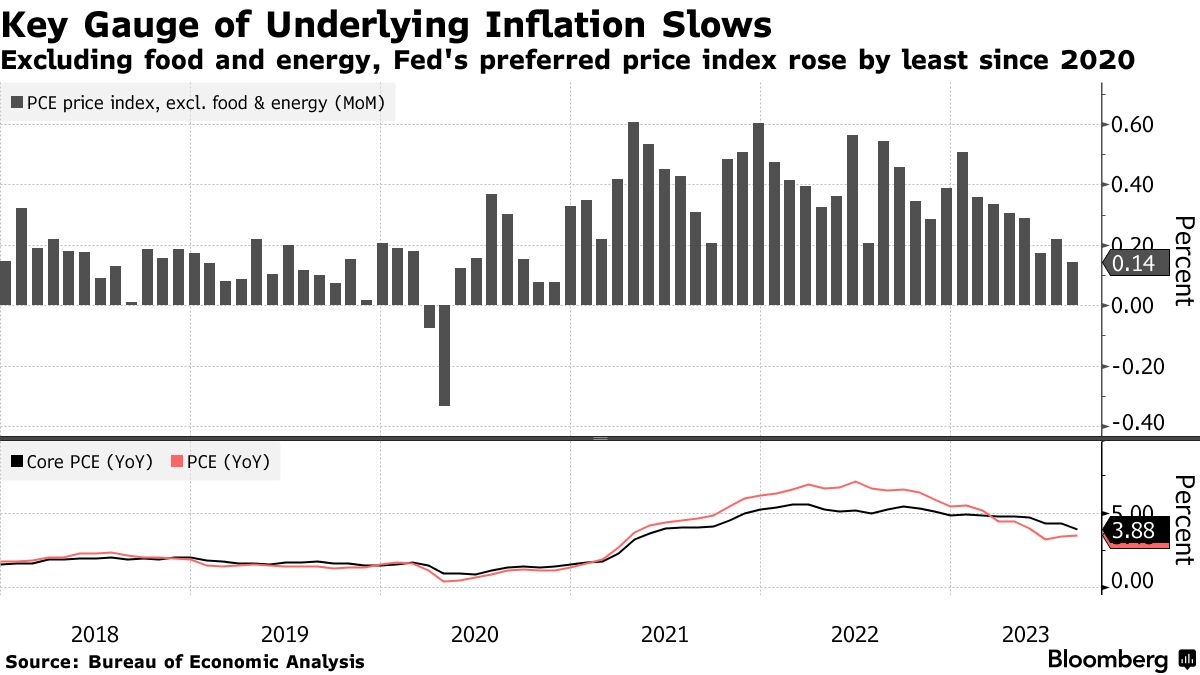

The Federal Reserve’s key gauge of underlying inflation rose at the slowest monthly pace since 2020. This illustrates to the powers that be that it is not rampant and the prevailing interest rates may be doing their job, which means rate hikes could slow, or even be at their peak. Excluding food and energy, the Fed’s preferred price index has slowed as seen in the chart below.

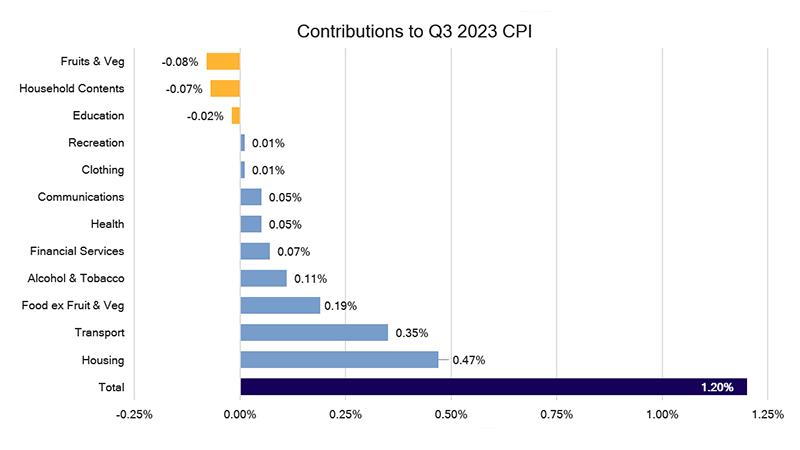

On the Australian front inflation still surprised a little on the upside. Here you can see a breakdown of the ABS’s latest inflation data:

Source: Australian Bureau of Statistics

The September quarter inflation number came out at 1.2% for both headline and underlying (trimmed mean) measures. This was above expectations of 1.1% and 1% respectively. In terms of headline inflation, it’s now fair to say the current pace is about 4% annually according to Investment managers, Pendal.

4. Hard landing versus soft landing

At the start of the year economists and market commentators stated that global economies in 2023 would have a hard landing as a result of the interest rate hikes and go into a recession. As time has passed and inflation has proved resilient, the same economists and market commentators feel a recession will be avoided, and we will experience a more gradual, softer economic landing, and avoid a recession.

5. Market Volatility & Timing the Market

With the changing of narratives, markets are understandably anxious.

At the start of the year the view was that interest rates would come down more quickly due to global economies going into recession, and therefore it would be better for companies, as interest rates would go down in a hard landing scenario and the equity risk premium for shares would be higher.

With interest rates staying higher for longer the equity risk premium shrinks and companies make less profit, which drives the share market lower. As economic growth slows, rates will go back down, which then leads to an increase in profit and share market gains.

So why not just time the market and get out?

If you invested $10,000 in the ASX200 on 31/10/2003 and left it invested through the Tech wreck of early 2000’s, the GFC, Covid, and what is happening now, you would have $49,410. If you missed just the 10 best trading days over that 20 year period, you would have $29,278. Thai is around a 40% difference from missing just 10 trading days. The biggest gains come when it is most volatile.

Interestingly let’s look at the following table as at 4/10/2023

Timing the Market

| Days invested | Ending Value on $10,000 initial investment | Behaviour Cost of Missing Best Days |

| Fully Invested | $49,410 | $0 |

| Missed 10 best days | $29,278 | $20,131 |

| Missed 20 best days | $19,385 | $30,024 |

| Missed 30 best days | $13,434 | $35,975 |

| Missed 40 best days | $9,715 | $39,695 |

6. Returns are unpredictable

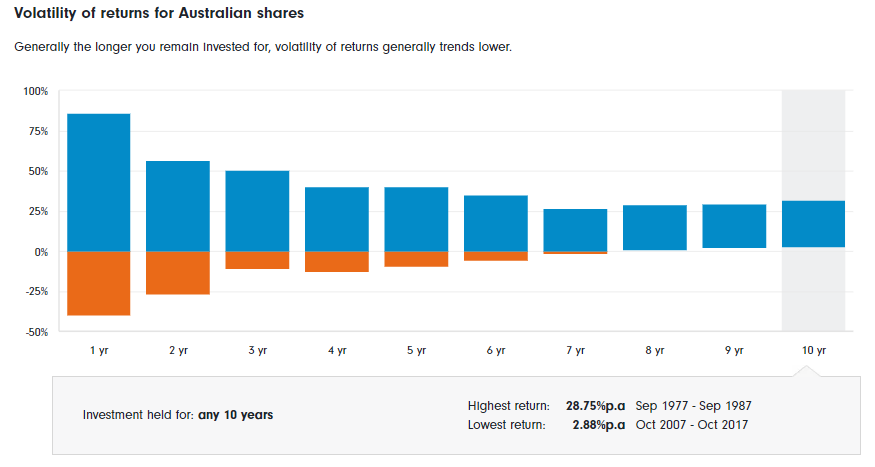

Over the short term returns are unpredictable. The ASX 200s worst 1 year return was -39.95% from Nov 2007 to Nov 2008 when the GFC hit. The single best 1 year return was 86.13% from Jul 1986 to July 1987.

Over the longer term you can see the dispersion comes in drastically with the worst 10 year return being 2.88% from Oct 2007 to Oct 2017. The best 10 year return is 28.75% from Sep 1977 to Sep 1987.

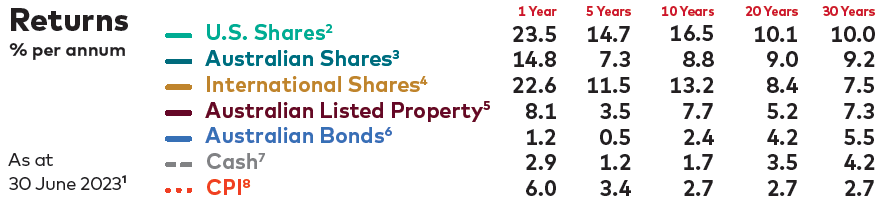

The average return on the ASX 200 is still well in excess of 9.2% per annum since 1993.

7. Cash is King isn’t it!

Not really. The RBA cash rate is 4.1% and the rate of inflation is around 5.3% so the maths on that is that you earn 4.1% p/annum but everything you are buying is going up by 5.3% p/annum. You are losing 1.2% of your purchasing power by putting money in the bank.

It would be a different story if the RBA cash rate was 4.1% and inflation was 2.0%. Then you would be getting a benefit of 2.1% each year which is okay, not great, but okay.

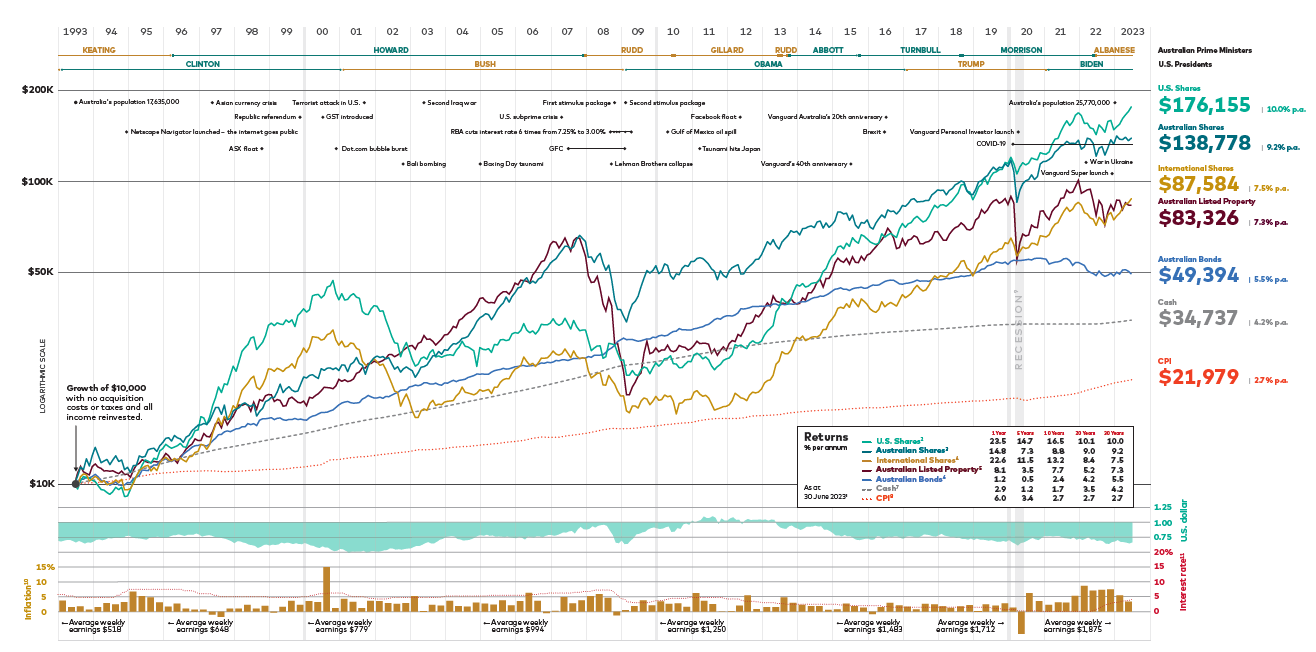

The Long term chart shows investment returns from 1 July 1993 to 30 June 2023. Not surprisingly shares were the better performing asset class over the 30 year time frame. As well as the 20 year, 10 year, 5 year and even 1 year.

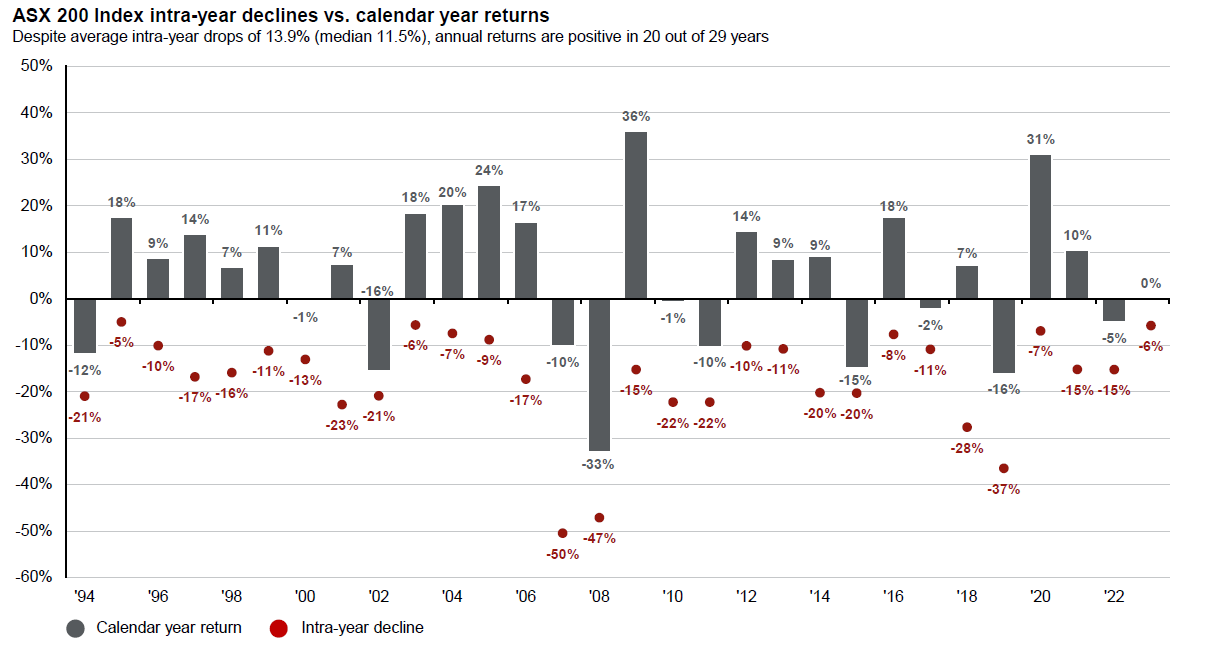

8. Annual share market returns and intra-year declines

A year comprises around 250 trading days and if you look at the chart below you can see the red dot is the worst return within the year, the intra-year. And the grey bar is the actual return you got for that year.

As an example in 2020 the sharemarket went down as much as -7% within the year, but for the entire year you got a return of 31%. This illustrates don’t panic within the year when there is volatility. Volatility is normal. Out of this data set there are positive returns 20 out of 29 years which means 69% of the time it is a positive year.

9. Longer term money being invested looks like this.

You can see that over the long term the growth assets of shares and properties far outweigh the returns from cash and bonds. With life expectancies increasing people are living longer so holding a portion of your wealth in growth assets makes sense.

Download the chart here for more information

10. What are we doing on the investment front

The key things we are doing right now in addition to reviewing your investment portfolio is:

- Staying up to date with economic news

- Meeting with managers to discuss how they are positioning portfolios

- Reviewing asset allocation

- Reviewing investment strategies

We will continue to keep our clients updated on what is happening on the investment front and as always, please reach out to our team if you have concerns or questions.