It’s been a long time coming, but up to 630,000 retirees could soon enjoy a small but welcome increase in their Age Pension payments following a cut in deeming rates used for the pension income test.i

Under the Age Pension income test, you are ‘deemed’ to earn a certain rate of interest on your savings and investments no matter how much income you actually receive.

The federal government announced in July that it will cut the lower deeming rate from 1.75 per cent to 1 per cent for financial investments worth up to $51,800 for single pensioners and $86,200 for pensioner couples where at least one person receives a pension. The upper deeming rate for savings above these thresholds will be cut from 3.25 per cent to 3 per cent.ii

As a result, Treasurer Josh Frydenberg said single pensioners could be better off by up to $804 a year and couples by up to just over $1,000.

Eligible pensioners will begin to receive the benefits from 20 September 2019 when pensions are next adjusted, but any extra payments will be backdated to July 1.

How does deeming work?

The deeming rules apply to income from financial assets such as superannuation (where the individual has reached age pension age), shares, savings accounts, term deposits and other fixed interest investments.

Different deeming rates apply if you are single or live with a partner.

To be eligible for the full Age or Veteran’s Affairs Pension under the income test, a single person can earn up to $174 a fortnight ($4,524 a year) before losing some of their pension. Couples can earn up to a combined $308 a fortnight ($8,008 a year).

For every $1 you earn over the threshold you lose 50c in pension income.

In other words, a single pensioner who has no other sources of income can have investment assets worth around $185,000 (with deemed income of $4,524) and still receive the full Age Pension. You must also pass the assets test, have reached pension age and be an Australian resident. Couples can have investments assets worth around a combined $324,000 (deemed to earn income just below $8,008) and receive the full pension.

Once your financial assets reach a certain threshold, your pension eligibility will be determined by the assets test rather than the income test. Single homeowners can have assets of up to $263,250 before their pension is reduced ($473,750 for non-homeowners). Home-owning couples can have $394,500 combined ($605,000 for non-homeowners).

Who is most affected?

Because of the complex interplay between the Age Pension income and assets tests, your relationship status and whether you own your home, the people most affected by deeming rates are part-pensioners.

Seniors advocate COTA Australia estimates that around 25 per cent of age pensioners are affected by deeming rates.iii Many of these have large sums in bank term deposits where interest rates have been steadily falling.

With official interest rates at a record low of 1 per cent, Age Pensioners who depend on income from cash investments face a double whammy. Not only do they receive less income from their bank deposits as interest rates fall, but they also risk losing some pension because they are deemed to earn more than they do.

The best term deposit rates are currently around 2.2%, but typically below 2% from the big banks. While the reduction in the top deeming rate from 3.25 per cent to 3 per cent is a help, it is still significantly higher than the return many retirees are earning.

Until the recent cut to deeming rates was announced, they had not moved since 2015. Since then, the Reserve Bank has cut the official cash rate five times, most recently in July, to a new historic low of 1 per cent with further cuts expected.

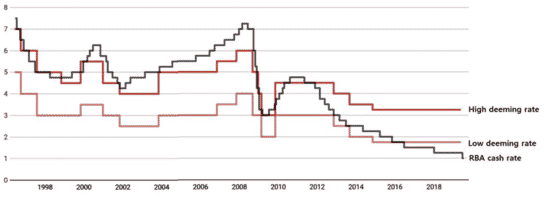

Deeming rates versus RBA cash rate, July 1996 – July 2019, per cent

Source: The Conversation

As the graph shows, deeming rates have been left well above the cash rate. That’s why pensioners were protesting before deeming rates were adjusted.

But there are also winners from the current level of deeming rates.

Winners and losers

Single pensioners with less than $51,800 in term deposits, and pensioner couples with less than $86,200, are probably earning a better rate of interest than the lower deeming rate of 1 per cent.

Even better off are retirees with money invested in Australian shares (either owned directly or within managed funds or superannuation) where yields have been over 4 per cent.iv This is significantly higher than the top deeming rate of 3 per cent.

Growth investments such as shares not only provide the opportunity to grow your capital over the long term, they pay regular income in the form of dividends along the way.

It’s understandable that retirees are risk averse and want to protect their capital. Bank term deposits provide the certainty of capital protection with a reliable income stream. But there is also an argument for diversifying your sources of income once you have covered your needs for ready cash.

If you would like to discuss your investment strategy in the light of changes to deeming rates and your Age Pension entitlements, give us a call.

i Treasurer Josh Frydenberg speaking on ABC TV, 14 July 2019, https://www.abc.net.au/news/2019-07-14/federal-government-announces-600-million-pension-boost/11307454

ii https://www.humanservices.gov.au/individuals/news/changes-deeming-rates

iii COTA Australia, 14 July 2019, https://www.cota.org.au/news-items/media-release-welcome-relief-on-pension-deeming-rates-council-on-the-ageing-will-continue-discussions-with-government-on-improving-the-process-in-future/

iv ASX Market Index, All Ords average dividend yield, https://www.marketindex.com.au/statistics. CoreLogic, gross rental yields in year to June 2019 were 4.1%, https://www.corelogic.com.au/sites/default/files/2019-07/CoreLogic%20home%20value%20index%20JULY%202019%20FINAL.pdf