Decisions around aged care are always difficult and emotional. From the start of next year they are likely to get even more complex, with both the Age Pension and aged care sectors set for another shake-up.

Currently, many people entering aged care choose to keep their former home and rent it out to help supplement their accommodation payments. From a financial planning perspective this strategy is attractive, as your former home and any rental income are exempt from assessment for the Age Pension. But from 1 January 2017 this will all change.

Changes to aged care fees

In recent years, the government has begun tightening the rules around the calculation of means-tested fees for residential aged care.

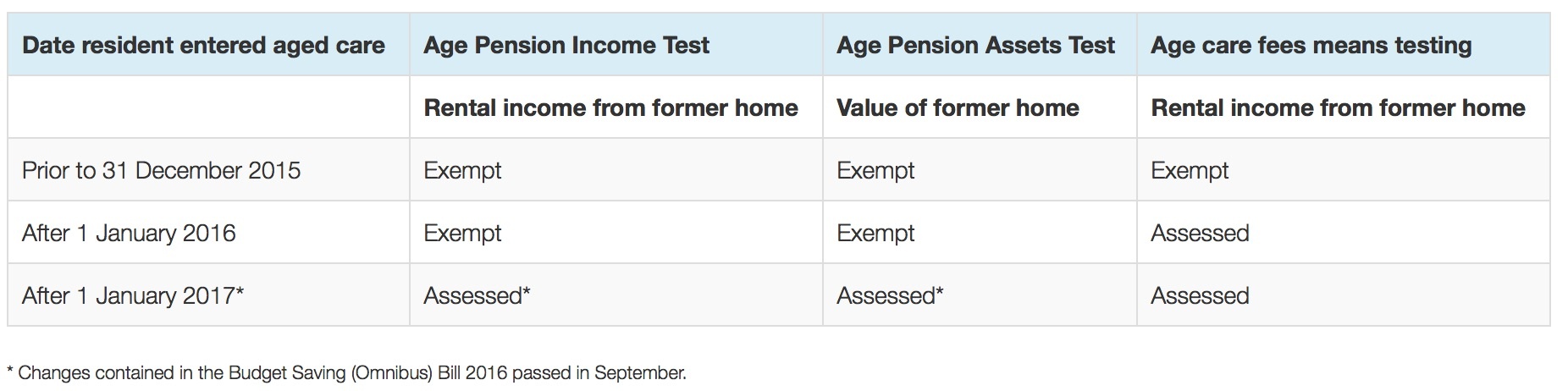

From 1 July 2014, both your assets and income were considered when calculating your aged care fee. However, if you retained your former home and chose to rent it out, the rental income was not counted towards your assessed income if you paid for some of your aged care costs using periodic payments, such as the rental-type ‘daily accommodation payment’.

On 1 January 2016 this rule changed, so when you entered aged care any rental income you received from your former home was included in your assessed income in the same way as any other type of income, such as interest or share dividends. Paying for your aged care costs using a periodic payment no longer had an advantage compared to paying via a lump sum.

These changes have seen many new residents of aged care facilities facing higher fees, as the assessable income used to calculate their fee is higher than under the pre-2016 rules.

Although these changes have affected aged care fees for new residents, they had no impact on the treatment of a former home when working out eligibility for the Age Pension. However, that’s now set to change.

Former home to be assessable for Age Pension

Currently, your former home is excluded from the Age Pension asset test for two years if you enter aged care. An indefinite exemption is available if your home is rented and you pay your accommodation costs with a periodic payment. In this situation, neither your former home nor the rental income are counted under the Age Pension asset or income tests.

This will change from 1 January 2017, when new amendments to legislation will harmonise the means-tested treatment of a former home for both aged care and the Age Pension.

According to the Treasurer, Scott Morrison, the changes will “align the pension means-testing arrangements with residential aged care arrangements. This measure removes poorly targeted exemptions that are associated with the pensioner’s former home, and are only available to pensioners who pay their aged care accommodation costs in periodic payments.”i

What this means for new entrants into aged care facilities is that the net rental income earned on your former home (where you decide to pay your accommodation costs with a daily payment rather than a lump sum), will now be counted towards the Age Pension income test.

Means-testing for aged care residents who rent their former home and fund their accommodation costs by periodic payments

Buy or sell your home?

With the new laws the decision about whether to keep your former home and rent it out will become more complicated for people entering residential aged care.

Under the old rules there were benefits in keeping your home, enjoying a boost to your income from any rental payments and making periodic payments. Now the decision will not be as straightforward.

Retaining your former home may still be worthwhile, but new aged care residents will need to carefully work out whether the benefit from their rental income outweighs the potential loss of some of their Age Pension.

Tougher asset test rules

Just to complicate matters, the new rules are planned to come into force at the same time as separate changes affecting the assets test thresholds used to calculate pension entitlements. Although limits for the Age Pension asset test are increasing from 1 January 2017, the rate at which pensions are reduced once you exceed the threshold is also increasing. This will see some pensioners have their pension payments reduced or cancelled altogether.

Both changes are likely to have an adverse impact on the Age Pension entitlement of some people entering aged care who wish to retain their former home. So before you make any binding decisions be sure to carefully weigh up all your options.

Aged care is a very complex area, so it’s important to seek professional advice before making any decisions in this area. If you would like to discuss your aged care funding options, please call our office.

i http://sjm.ministers.treasury.gov.au/speech/016-2016/