What is superannuation?

We all have dreams of what we would like more of in retirement. More time for travel, to pursue other interests or to relax with family and friends. To ensure you get to enjoy more of what you dream about, you need to start a dedicated savings plan. And that’s where superannuation comes in.

Superannuation, or ‘super’, is a special type of investment account Australians use to save for retirement. Over your working life, money is contributed to a super fund. These funds invest in a variety of assets such as shares, property, bonds and cash and the money is then paid to you on retirement either as a lump sum or an income stream.

Employers pay compulsory super contributions on your behalf and these can be topped up by you or your spouse. If you are self-employed you can choose whether to contribute to super.

Check with your employer if you get to choose which super fund will receive your contributions. There are several types to choose from: an employer fund, an industry fund, a retail fund or a self-managed super fund. If you don’t choose, or are unable to choose, your employer will nominate a default fund.

Super receives generous tax concessions before and after you retire to encourage you to save for retirement. Contributions can be made either before or after tax but there are caps imposed on how much you can pay in each year.

Why is super important?

There are two sides to this coin. Super is important for you because it will help you achieve a better standard of living in your retirement years.

But it is also aimed at reducing dependence on the government’s aged pension, particularly in light of the growing number of baby boomers reaching retirement age.

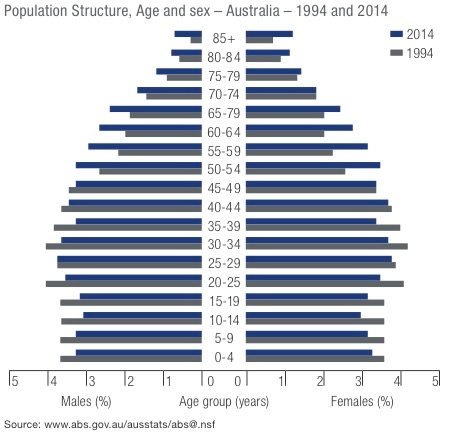

As the graph below shows, in the 20 years to June 2014 the proportion of Australians aged 65 years and over rose from 11.8 per cent to 14.7 per cent. This number is expected to increase more rapidly in the next 10 years.

How much super will you need?

The ASFA Retirement Standard estimates the annual budget needed for Australians to enjoy either a modest or comfortable lifestyle. The figure is updated quarterly.

By this measure a couple will need $640,000 in savings to achieve a comfortable lifestyle in retirement or $50,000 for a modest lifestyle. But a modest lifestyle is only marginally better than the age pension.

Of course, the amount you actually need will depend on your individual circumstances, what you expect from your retirement, the age at which you will retire and whether you have money invested outside super.

How can you contribute to super?

When you earn more than $450 a month, your employer will make what is called a superannuation guarantee contribution on your behalf. This currently stands at 9.5 per cent of your salary and is taxed at 15 per cent.

You can make additional pre-tax contributions by way of salary sacrifice, but there is a limit to the amount you can contribute each year. The general concessional cap is $30,000; if you are age 49 or over on 30 June 2015 it’s $35,000.

You can also make contributions from your after-tax money, known as a non-concessional contribution. This is subject to a cap of $180,000 a year although you can make a lump sum contribution of $540,000 over a three year rolling period as long as you are aged under 65.

All these caps are reviewed for indexation annually.

If your spouse is on a very low income then you may be able to make a non-concessional contribution on their behalf of up to a certain limit and claim a tax offset.

You may also be entitled to a government co- contribution of up to $500 if you earn less than an annually-adjusted amount and make a personal after- tax contribution.

How is super taxed?

Concessional pre-tax contributions are generally taxed at 15 per cent as they go into your super account, or 30 per cent if you earn more than $300,000 a year. This is often considerably less than your marginal tax rate.

Any earnings on your investments inside super are also taxed at 15 per cent while you are still working and accumulating savings. This rate can be reduced even further by using franking credits attached to the dividend income from shares.

If you are over preservation age (55-60 depending on your date of birth) there may be tax payable if you start to withdraw cash from your super. Once you turn 60, all monies taken out of super are tax Complimentary.

When can you access super?

The purpose of super is to fund your retirement so there are restrictions on when you can access the money. The minimum age you can access your super – referred to as your preservation age – is 55 years if you were born before 1960. It is gradually being increased until it hits 60 for those born 1965 or later.

Once you reach preservation age and retire permanently there are no restrictions on how much of your savings you can withdraw. Alternatively, you can continue working and withdraw some of your super as an income stream using a transition to retirement pension.

When you retire you can take your super as a lump sum or as an income stream. However, there is a strong argument for not taking a lump sum before you turn 60, when all withdrawals are tax Complimentary.

We can help you work out the best way to take advantage of super to fund the lifestyle you want in retirement.

{kind=link}